Saudi Arabia to extend 1 million barrel oil cut into October

- August 24, 2023

- Posted by: Quatro Strategies

- Categories: Business & Politics, Middle East, Oil & Gas

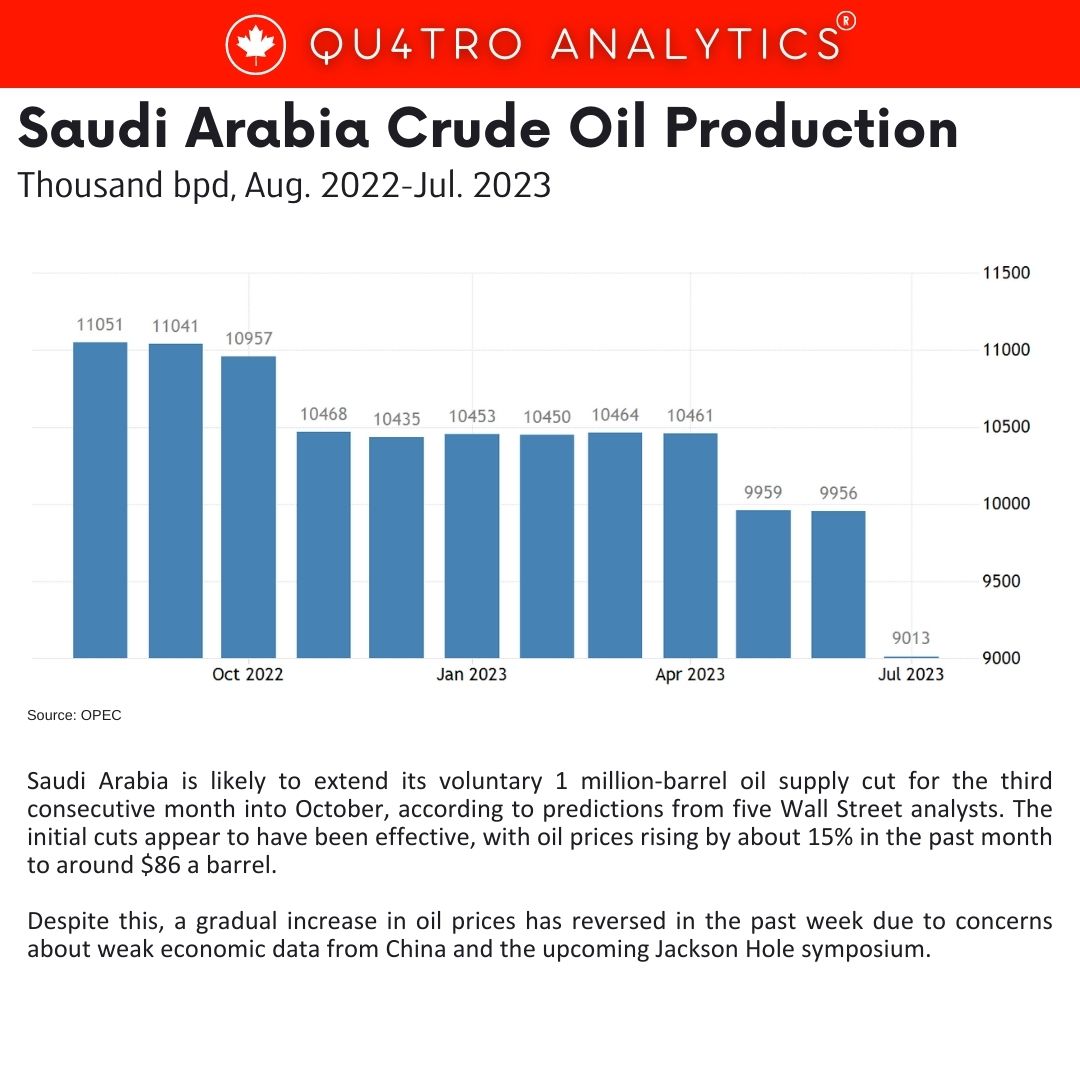

Saudi Arabia is likely to extend its voluntary 1 million-barrel oil supply cut for the third consecutive month into October, according to predictions from five Wall Street analysts. The initial cuts appear to have been effective, with oil prices rising by about 15% in the past month to around $86 a barrel. Despite this, a gradual increase in oil prices has reversed in the past week due to concerns about weak economic data from China and the upcoming Jackson Hole symposium.

The current Brent crude prices of $82.71 are considered too low for Saudi Arabia, as the country needs oil prices at around $100 a barrel to balance its fiscal budget. This provides the country with further incentive to maintain tight supplies in the market. Richard Bronze, an analyst at consultancy Energy Aspects, has stated that Saudi Arabia is likely to extend the supply cut through October. The cautious approach is influenced by the weaker oil market conditions in the first half of the year, and the country will want to see a significant decline in global inventories before considering unwinding the additional cuts.

Analysts from brokerage PVM Oil and Saxo Bank have also speculated that a potential resumption of oil production from Iraq’s Kurdistan region might lead Saudi Arabia to withhold additional supplies to the market for the time being. Despite these uncertainties, oil markets are expected to tighten gradually, leading to an increase in prices as the months progress.

Analysts from brokerage PVM Oil and Saxo Bank have also speculated that a potential resumption of oil production from Iraq’s Kurdistan region might lead Saudi Arabia to withhold additional supplies to the market for the time being. Despite these uncertainties, oil markets are expected to tighten gradually, leading to an increase in prices as the months progress.

The International Energy Agency (IEA) has predicted a global oil shortage of approximately 1.7 million barrels per day during the second half of the year. Experts at Standard Chartered have forecasted a supply deficit of 2.81 million barrels per day in August, 2.43 million barrels per day in September, and over 2 million barrels per day in November and December. Their projections also suggest that global inventories will decrease by 310 million barrels by the end of 2023 and another 94 million barrels in the first quarter of 2024, contributing to higher oil prices. The experts anticipate that Brent prices will rise to $93 per barrel in the fourth quarter.

Interested in learning more?

Sign up for Top Insights Today

Top Insights Today delivers the latest insights straight to your inbox.

You will get daily industry insights on

Oil & Gas, Rare Earths & Commodities, Mining & Metals, EVs & Battery Technology, ESG & Renewable Energy, AI & Semiconductors, Aerospace & Defense, Sanctions & Regulation, Business & Politics.

Read more insights

China’s raw material stockpiling surges amid economic challenges and energy transition

China’s current raw material inventory situation reflects both the country’s cautious approach to ensuring supply security and the impact of its economic challenges. The country has seen a dramatic increase in coal inventories, which surged to a record 635 million tons by mid-2024, up from under 90 million tons in late…

China’s demand for off-exchange copper soars, DRC becomes key supplier

China’s imports of off-exchange refined copper, particularly from the Democratic Republic of Congo (DRC), are set to increase in 2025 as demand continues to outstrip global supply. This trend reflects China’s growing reliance on Congolese copper production and the appeal of lower-cost equivalent grade (EQ) copper, which meets the same quality standards as exchange-registered copper but trades at a discount.

The surge in EQ copper imports highlights the shifting dynamics of the global copper trade. Last year, EQ copper accounted for 62% of China’s refined copper imports, up from just under half in 2022. This rise is largely driven by Congo’s expanding output, which has made it the world’s second-largest copper producer, thanks to significant Chinese investments in its mining sector.

Japan, China, South Korea, and ASEAN create new crisis lending mechanism

Japan, China, South Korea and the 10 ASEAN countries have agreed to launch a new emergency lending facility under their joint financial framework, aiming to bolster regional resilience against economic shocks stemming from pandemics or natural disasters.

The agreement was reached during a meeting of finance leaders from the so-called ASEAN Plus Three group in Milan, Italy. The new mechanism will operate within the existing Chiang Mai Initiative Multilateralization (CMIM) framework, a currency swap arrangement established in the aftermath of the 1997–1998 Asian financial crisis to enhance regional financial stability.