China’s economic recovery hopes reignite after slower than expected trade decline

- September 7, 2023

- Posted by: Quatro Strategies

- Categories: Business & Politics, China

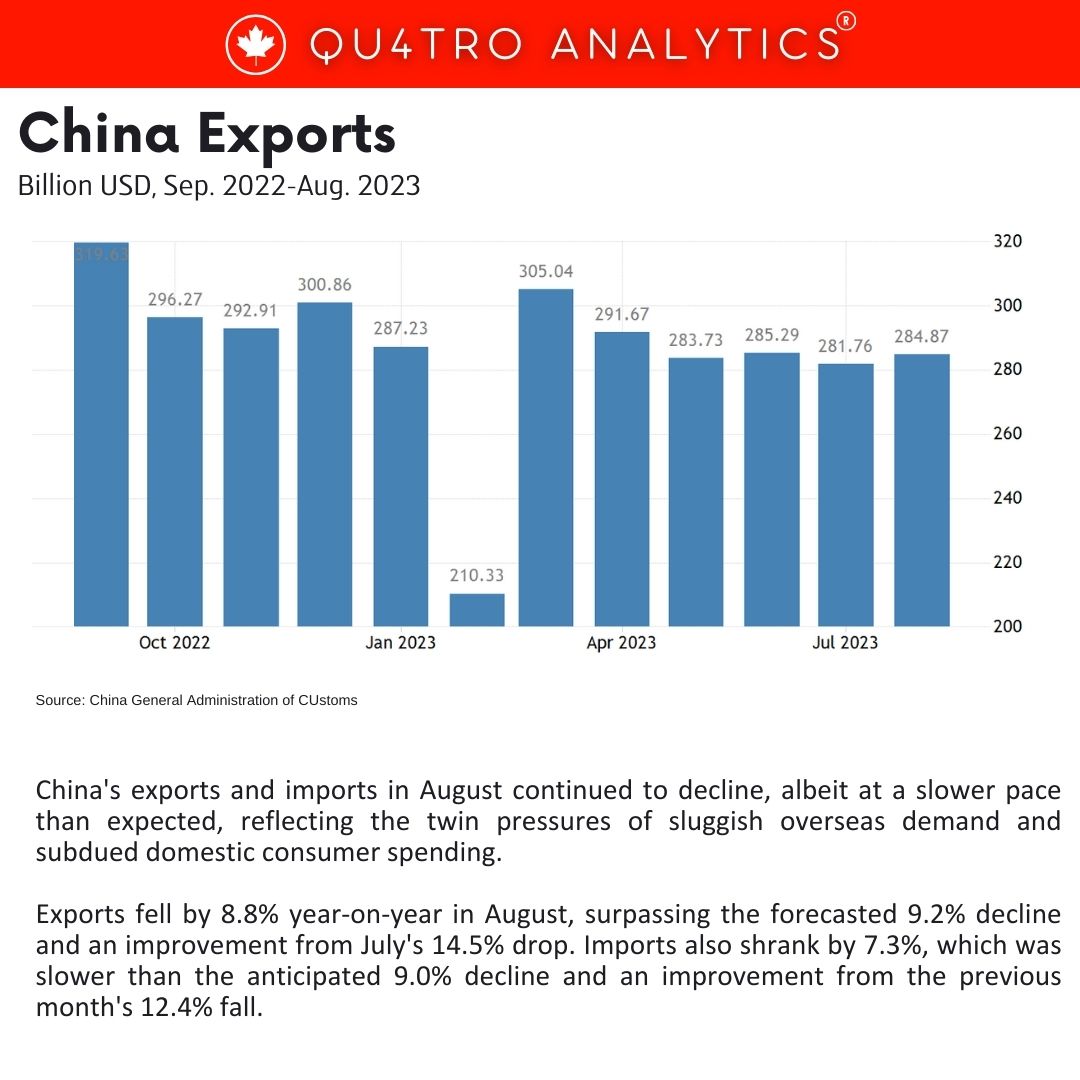

China’s exports and imports in August continued to decline, albeit at a slower pace than expected, reflecting the twin pressures of sluggish overseas demand and subdued domestic consumer spending. Exports fell by 8.8% year-on-year in August, surpassing the forecasted 9.2% decline and an improvement from July’s 14.5% drop. Imports also shrank by 7.3%, which was slower than the anticipated 9.0% decline and an improvement from the previous month’s 12.4% fall.

While the numbers suggest some stabilization in China’s economic downturn, they still fall short of the growth expectations earlier in the year when China eased strict COVID restrictions. China’s economy faces headwinds from a deepening property slump, weak consumer spending, and falling credit growth, leading to downgraded growth forecasts for the year.

Despite some marginal improvement, analysts caution that the situation remains challenging. Measures announced by Beijing to boost growth, such as easing borrowing rules, may have limited impact as the labor market recovery slows, and household income expectations remain uncertain.

The slowdown in China’s economic growth is a concern for governments worldwide, given their dependence on China’s market for their own growth. South Korean shipments to China, for example, slowed at a lesser rate in August, suggesting conditions may be stabilizing in China. However, Japan experienced a sharp drop in trade with China, impacting its fragile recovery.

The slowdown in China’s economic growth is a concern for governments worldwide, given their dependence on China’s market for their own growth. South Korean shipments to China, for example, slowed at a lesser rate in August, suggesting conditions may be stabilizing in China. However, Japan experienced a sharp drop in trade with China, impacting its fragile recovery.

Crude oil shipments to China increased by 31% in August compared to the same period the previous year, while soybean imports surged by 31% year-on-year, driven by competitive prices in Brazil.

While the data shows some signs of stabilization, the yuan remains near a 10-month low, and the Australian dollar, often seen as a proxy for Chinese growth, weakened after the release of the trade data. China’s trade surplus for August came in at $68.36 billion, below the forecasted $73.80 billion and down from July’s $80.6 billion.

Overall, the situation in China’s trade sector remains uncertain, and the country’s efforts to stimulate economic growth are being closely watched by policymakers and investors alike.

Interested in learning more?

Sign up for Top Insights Today

Top Insights Today delivers the latest insights straight to your inbox.

You will get daily industry insights on

Oil & Gas, Rare Earths & Commodities, Mining & Metals, EVs & Battery Technology, ESG & Renewable Energy, AI & Semiconductors, Aerospace & Defense, Sanctions & Regulation, Business & Politics.

Read more insights

Trump’s trade policies cast shadow over industrial precious metals market

The demand for industrial precious metals such as platinum and palladium is expected to decline if U.S. President Donald Trump follows through on his proposed tariffs on auto imports. Analysts predict that higher vehicle costs due to tariffs could dampen demand for cars in the U.S., leading to a ripple effect on platinum group metals (PGMs), which are critical for vehicle exhaust systems in gasoline, diesel, and hybrid vehicles.

Trump has indicated that these tariffs could take effect as early as April 2, making auto imports more expensive and potentially reducing the sales of foreign-made vehicles in the U.S. economy.

China tightens control over capital outflows and strategic technology

China’s new outbound investment directive marks a significant tightening of Beijing’s control over how Chinese capital, technology, data and expertise move abroad. The regulation, issued by the State Council and set to take effect on July 1, is designed to strengthen national security reviews of overseas investments and consolidate a patchwork of existing rules that had been spread across agencies such as the National Development and Reform Commission, the Ministry of Commerce and the State Administration of Foreign Exchange.

In practical terms, it gives Beijing more power to decide which foreign deals Chinese companies and individuals can pursue, especially when those deals involve sensitive technology, data, services or strategic assets.

As LNG prices surge, Asian utilities pivot back to cheaper coal

Escalating conflict in the Middle East is unexpectedly strengthening the position of thermal coal in global energy markets, particularly in Asia, as liquefied natural gas (LNG) prices climb in response to geopolitical risk. The sharp rise in LNG spot prices has made coal more economically attractive in markets where utilities can switch between fuels—most notably Japan and South Korea.

The conflict, initially between Israel and Iran and now involving the United States, has heightened concerns about potential disruptions to global energy flows through the Strait of Hormuz—a critical chokepoint for both crude oil and LNG. Nearly 20% of the world’s seaborne LNG, primarily from Qatar, transits through this narrow waterway.