France’s Orano suspends uranium processing operations in Niger

- September 14, 2023

- Posted by: Quatro Strategies

- Categories: Africa, Europe, Mining & Metals

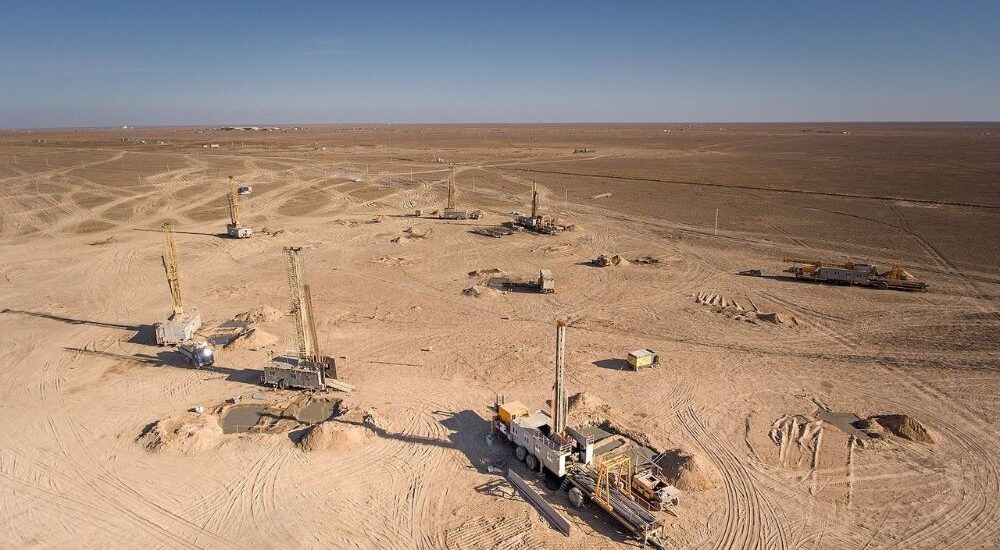

French nuclear group Orano SA is suspending uranium ore processing at one of its facilities in Niger due to international sanctions against the military junta, which are affecting logistics. This move could potentially tighten supplies of uranium used to fuel nuclear reactors in several countries, including the US, China, and Europe, and force utilities to rely more on other producers like Kazakhstan, Canada, and Australia.

Orano’s uranium treatment plant in Niger was originally scheduled for maintenance early next year, but it has been moved forward due to depleting stockpiles of the chemicals needed for processing. Operations are continuing at Orano’s Somair mine, which is partially owned by the Niger government.

Orano typically exports uranium concentrate to Benin, where it is shipped either back to France or to Canada. There are usually 4-6 shipments per year.

To secure supply for its customers, Orano is also sourcing material from mines in Canada and Kazakhstan, where it holds stakes. In the short term, there is no emergency, but the situation highlights the potential impact of geopolitical events on the global uranium supply chain.

Interested in learning more?

Sign up for Top Insights Today

Top Insights Today delivers the latest insights straight to your inbox.

You will get daily industry insights on

Oil & Gas, Rare Earths & Commodities, Mining & Metals, EVs & Battery Technology, ESG & Renewable Energy, AI & Semiconductors, Aerospace & Defense, Sanctions & Regulation, Business & Politics.

Read more insights

Equinor to hold Norway’s oil and gas line into the 2030s

Equinor is essentially betting that the world will still want a lot of oil and gas well into the 2030s and beyond, and it’s reorganising Norway’s offshore sector around that assumption. The company’s CEO, Anders Opedal, has laid out a plan to drill about 250 new exploration wells on the Norwegian continental shelf over the next decade, with annual investment of around 60 billion Norwegian crowns, roughly $6 billion a year.

The explicit goal is to keep Equinor’s production in 2035 at roughly the same level it was in 2020, despite the natural decline of mature fields. On an ageing shelf where output would normally fall steadily, that is a very ambitious industrial mobilisation, and Opedal himself described it as one of the biggest industrial efforts in Norway’s history rather than “business as usual.”

Anti-dumping duty turns U.S. anode localization from aspiration to imperative

India’s Epsilon Advanced Materials is moving quickly to exploit a sudden opening in the U.S. battery supply chain after Washington slapped a 93.5% anti-dumping duty on Chinese graphite anode materials. With Chinese inputs now far less economical, Japanese and South Korean battery makers operating in the U.S. have shifted from “wait and see” to active procurement, and Epsilon says it expects to lock in contracts within the next two to three months.

Those offtakes would underpin a $650 million plant in North Carolina, sized for 30,000 tonnes a year of anode material and slated to start up by mid-2027. It’s a meaningful first step but still small versus an estimated 500,000 tonnes the U.S. market needs annually, demand that until now was met largely with material refined in China, which controls over 90% of global graphite processing.

China steel production hits seven-year low; exports keep rising

China’s steel sector is entering 2026 with a familiar structural problem: domestic demand is still anchored to a weak property market, so mills are increasingly leaning on product-mix optimization and exports to keep utilization and margins from collapsing.

Crude steel production fell to 960.81 million metric tons in 2025, dropping below one billion tons for the first time in years and marking the lowest annual level since 2018. The 4.4% decline from 2024 underscores how the protracted real-estate downturn continues to compress the country’s traditional steel demand base, especially in construction-intensive categories.