Nigeria to establish state-backed mineral company to boost investments

- September 4, 2023

- Posted by: Quatro Strategies

- Categories: Africa, Mining & Metals, Rare Earths & Commodities

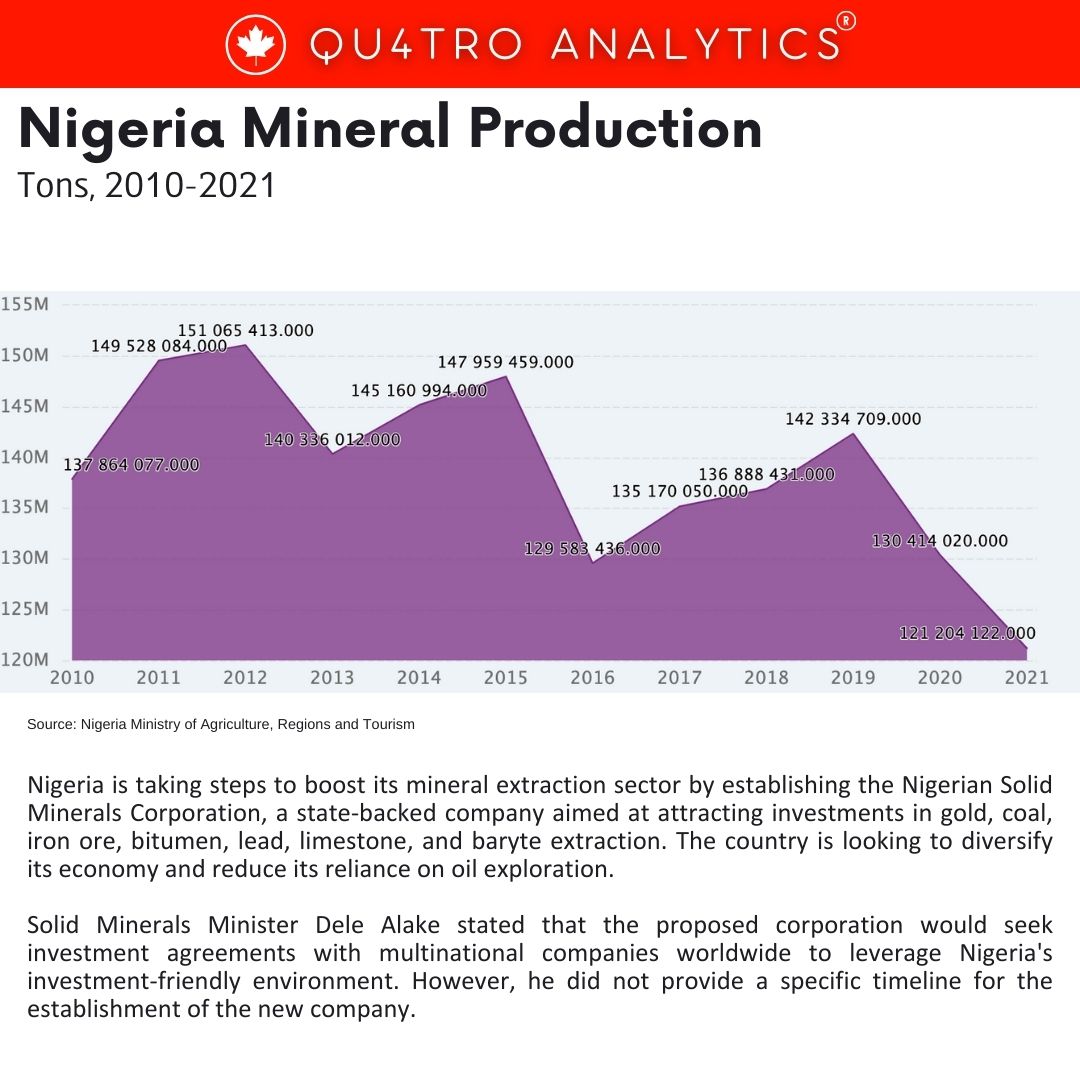

Nigeria is taking steps to boost its mineral extraction sector by establishing the Nigerian Solid Minerals Corporation, a state-backed company aimed at attracting investments in gold, coal, iron ore, bitumen, lead, limestone, and baryte extraction. The country is looking to diversify its economy and reduce its reliance on oil exploration.

Solid Minerals Minister Dele Alake stated that the proposed corporation would seek investment agreements with multinational companies worldwide to leverage Nigeria’s investment-friendly environment. However, he did not provide a specific timeline for the establishment of the new company.

Existing entities like the National Iron Ore Company and the Bitumen Concessioning Programme will be reviewed and incorporated into the new corporation. Additionally, a mines police force will be operational from October to combat illegal mining activities.

Existing entities like the National Iron Ore Company and the Bitumen Concessioning Programme will be reviewed and incorporated into the new corporation. Additionally, a mines police force will be operational from October to combat illegal mining activities.

President Bola Tinubu’s administration is implementing reforms to improve Nigeria’s investment climate and attract foreign investors. These reforms aim to shift the focus from borrowing to investment as a means of creating jobs and stimulating economic growth. Tinubu plans to attend the upcoming G20 summit to promote foreign investment in Nigeria and secure global capital for infrastructure development.

The Nigerian Solid Minerals Corporation will collaborate with local financial institutions, encouraging them to invest in the mining sector, which has historically faced challenges due to lengthy project gestation periods. The move represents part of Nigeria’s broader efforts to diversify its economy and tap into its vast mineral resources.

Interested in learning more?

Sign up for Top Insights Today

Top Insights Today delivers the latest insights straight to your inbox.

You will get daily industry insights on

Oil & Gas, Rare Earths & Commodities, Mining & Metals, EVs & Battery Technology, ESG & Renewable Energy, AI & Semiconductors, Aerospace & Defense, Sanctions & Regulation, Business & Politics.

Read more insights

China’s oil demand growth to slow down amid accelerated decarbonization efforts

China’s oil demand has entered a phase of low growth as the country accelerates its decarbonization efforts, according to China National Petroleum Corp., the nation’s largest energy producer. Lu Ruquan, president of CNPC’s Economics & Technology Research Institute, stated that the increasing…

China’s demand weakness turns industrial strength into a political liability

The micro-level retrenchment maps onto a broader imbalance that has become China’s defining economic problem: households and small businesses are cautious, while factories and industrial ecosystems continue to produce at scale.

When consumption is weak but supply keeps expanding, the clearing mechanism is usually price. Companies discount to move inventory, profits compress, and investment returns deteriorate. That, in turn, encourages employers to cap wages, slow hiring, or cut staff, which reduces household income growth and reinforces consumer restraint.

Elections in 2024 marks a year of political significance for markets

In the upcoming year, elections in countries representing a significant portion of the global economy and population are poised to have notable implications for financial markets. These impending elections underscore the potential for significant market movements in response to political outcomes…