Uranium demand for nuclear reactors expected to double by 2040

- September 8, 2023

- Posted by: Quatro Strategies

- Categories: Mining & Metals, Rare Earths & Commodities

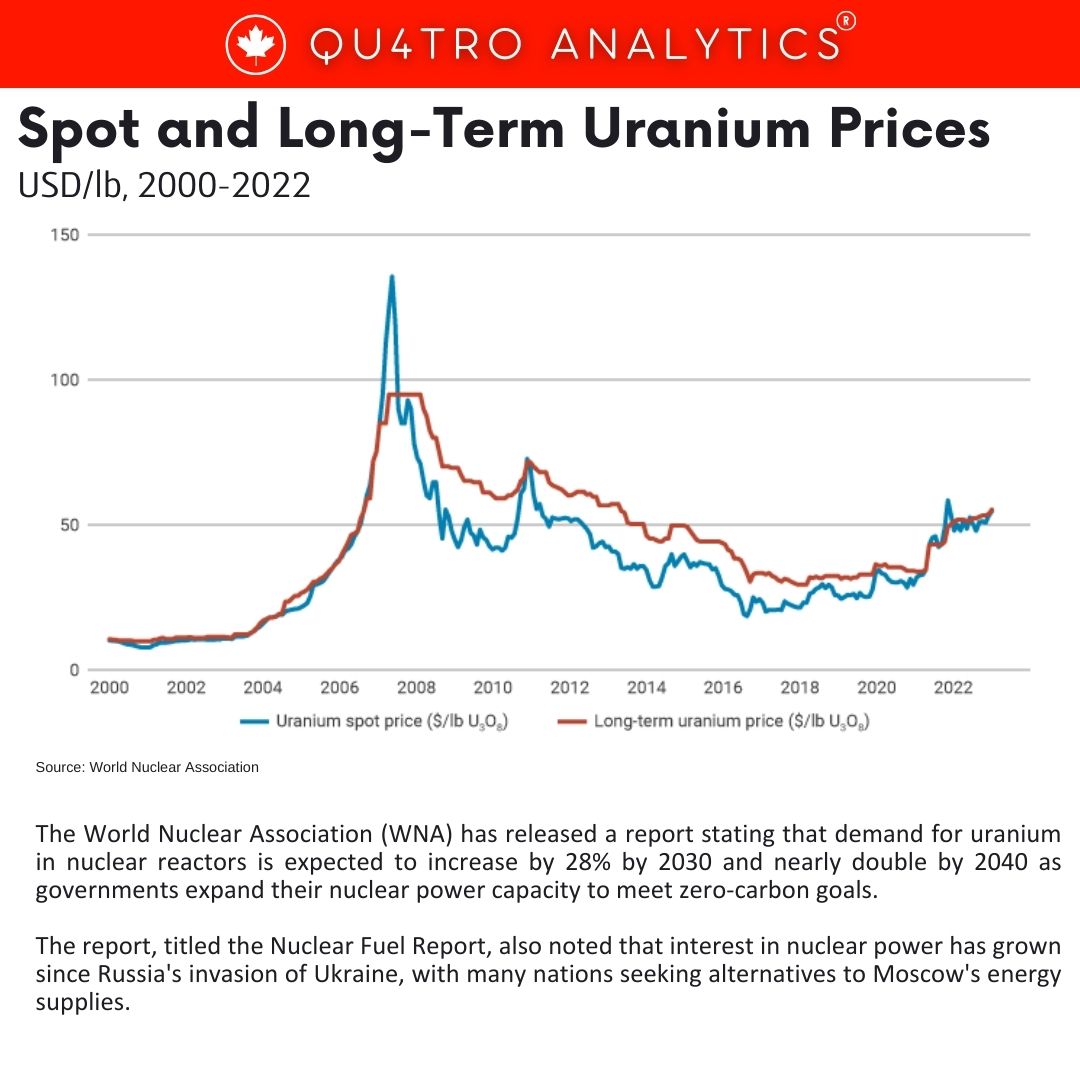

The World Nuclear Association (WNA) has released a report stating that demand for uranium in nuclear reactors is expected to increase by 28% by 2030 and nearly double by 2040 as governments expand their nuclear power capacity to meet zero-carbon goals. The report, titled the Nuclear Fuel Report, also noted that interest in nuclear power has grown since Russia’s invasion of Ukraine, with many nations seeking alternatives to Moscow’s energy supplies.

The report highlights that, “From the beginning of the next decade, planned mines and prospective mines, in addition to increasing quantities of unspecified supply, will need to be brought into production.” Global uranium production had declined by 25% from 2016 to 2020 but slightly recovered to 49,355 tonnes in 2021.

The Fukushima Daiichi nuclear disaster in Japan in 2011 led to the closure of numerous reactors worldwide. However, global nuclear capacity at the end of June 2023 was 391 gigawatts of electricity (GWe) from 437 units, with an additional 64 GWe under construction. Nuclear capacity is projected to increase by 14% by 2030 and surge by 76% to reach 686 GWe by 2040.

This capacity expansion will come from both new reactors, primarily planned in China and India, and the extension of the operating lifetimes of existing plants. The report highlights that several countries with significant reactor fleets, such as Canada, France, Japan, Russia, and Ukraine, are allowing existing plants to operate for up to 60 years, with the USA allowing up to 80 years.

This capacity expansion will come from both new reactors, primarily planned in China and India, and the extension of the operating lifetimes of existing plants. The report highlights that several countries with significant reactor fleets, such as Canada, France, Japan, Russia, and Ukraine, are allowing existing plants to operate for up to 60 years, with the USA allowing up to 80 years.

Small modular reactors (SMRs), which are easier and more cost-effective to build, are also gaining traction. The WNA report forecasts that demand for uranium for nuclear plants will rise to 83,840 tonnes by 2030 and 130,000 tonnes by 2040, up from 65,650 tonnes in 2023.

The spot price of uranium has more than doubled over the past three years, although it remains significantly below its peak of $140 per pound in 2007. As of this week, uranium is trading at $60.75 per pound, up from $56.25 a month ago, according to market research firm and consultancy UxC.

Interested in learning more?

Sign up for Top Insights Today

Top Insights Today delivers the latest insights straight to your inbox.

You will get daily industry insights on

Oil & Gas, Rare Earths & Commodities, Mining & Metals, EVs & Battery Technology, ESG & Renewable Energy, AI & Semiconductors, Aerospace & Defense, Sanctions & Regulation, Business & Politics.

Read more insights

ExxonMobil gears up for commercial operations at $10 billion China petrochemical hub

ExxonMobil has begun securing shipments of naphtha for its newly launched petrochemical complex in southern China, as the U.S. energy giant prepares for the official start-up of its $10 billion plant. The move is expected to boost regional demand for petrochemical feedstock and strengthen Asian naphtha refining margins, which are already benefiting from reduced Russian supply.

Located in the Dayawan Petrochemical Industrial Park in Huizhou, Guangdong province, the complex is one of the few wholly foreign-owned mega petrochemical facilities in China, designed to produce high-end petrochemical products.

Rising interest rates prompt short sales of oil despite conflict in the Middle East

Portfolio investors have resumed selling petroleum as concerns about rising interest rates and their impact on the global economy have taken precedence over earlier fears of conflict in the Middle East disrupting oil production. Hedge funds and other money managers…

Aluminium faces soft demand but tight supply keeps price floor intact

Aluminium prices are under pressure in 2025 as global demand softens amid ongoing trade tensions and economic uncertainty, but analysts say downside risks are likely to be capped by structural limits on Chinese output and a relatively tight global supply-demand balance.

Since rising 7% last year, aluminium prices on the London Metal Exchange (LME) have slipped 2% year-to-date, primarily due to weaker demand from key sectors such as transport, construction, and renewable energy—all of which are sensitive to broader macroeconomic shifts. The tariff standoff between the United States and China has further dampened confidence, with importers and manufacturers holding back on purchases amid an unpredictable trade environment.